Oil:

- Over the past weekend, there were a series of mutual attacks between Ukraine and Russia, which is increasing geopolitical risk and supporting the recent rebound in oil prices.

- OPEC+ agreed to raise production by 411,000 barrels per day in July, similar to the previous two months.

- Before the weekend, there was information that a larger production increase might occur, which led to prices falling to their lowest level since May 8. However, the first session of June brings a clear recovery. Brent crude is back above $65 per barrel, while WTI crude is testing the $63 per barrel area.

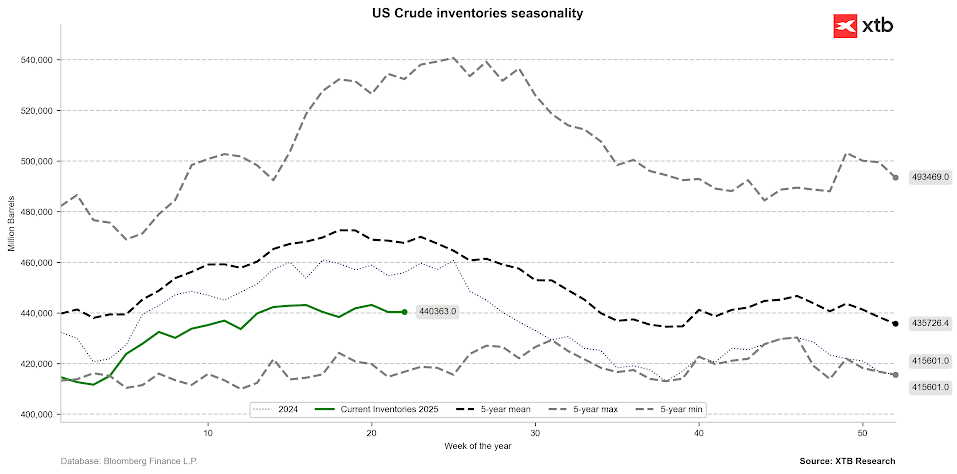

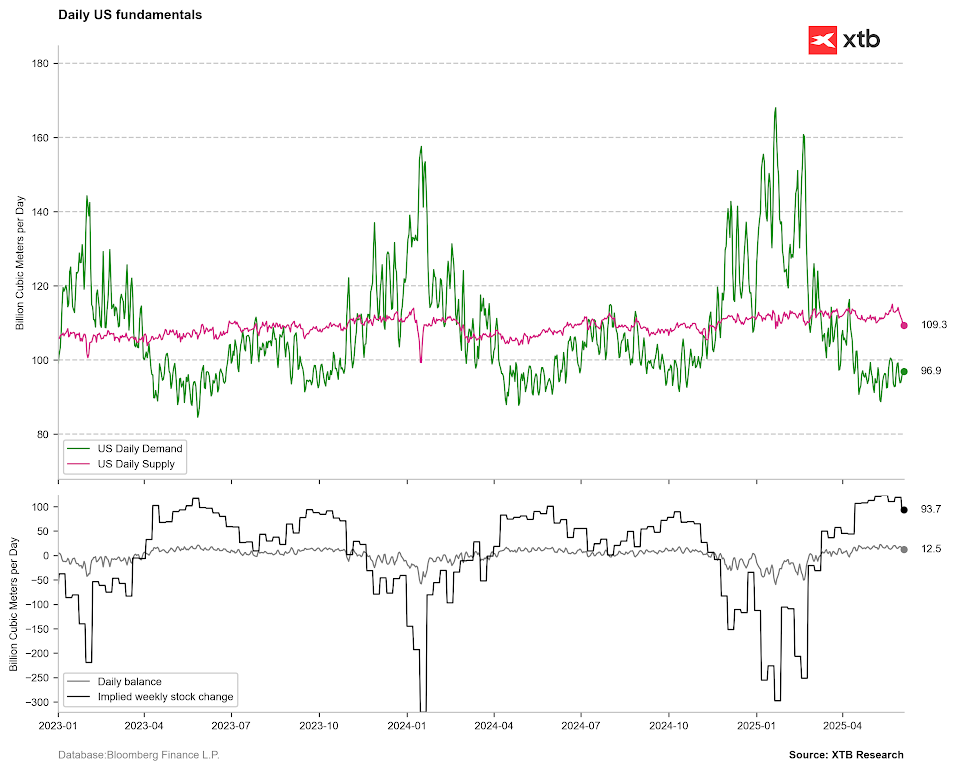

- US crude oil inventories have remained stable in recent weeks. Seasonality already points to declines, but the current stability in inventories looks similar to last year. It’s worth remembering that the market currently has an oversupply.

US crude oil inventories have remained stable in recent weeks. While seasonality suggests declines, the current stability in inventories mirrors last year’s trend. It’s important to remember that the market is currently experiencing an oversupply. Source: Bloomberg Finance L.P., XTB Research

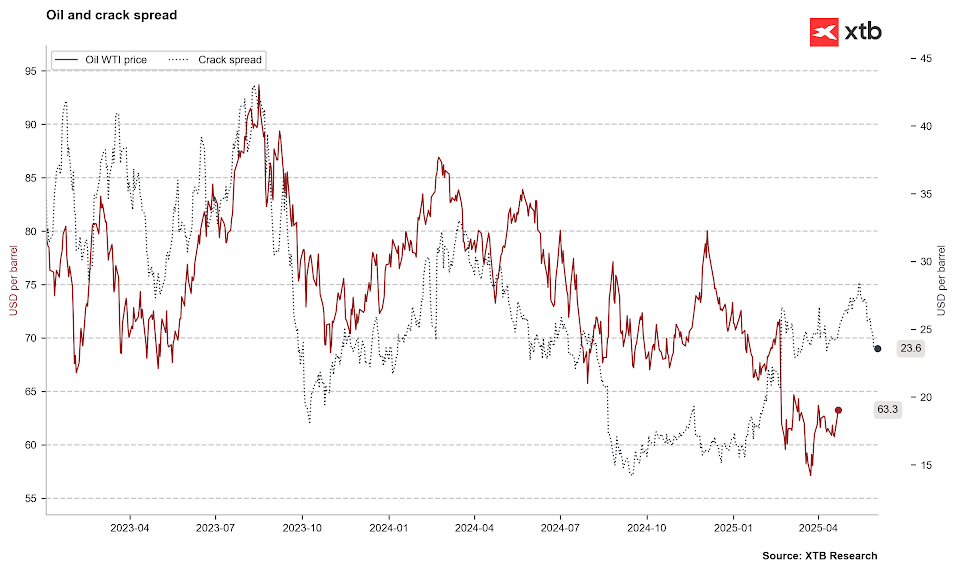

The margin on refined petroleum products has begun to decline slightly, but it still remains at an elevated level. Source: Bloomberg Finance L.P., XTB Research

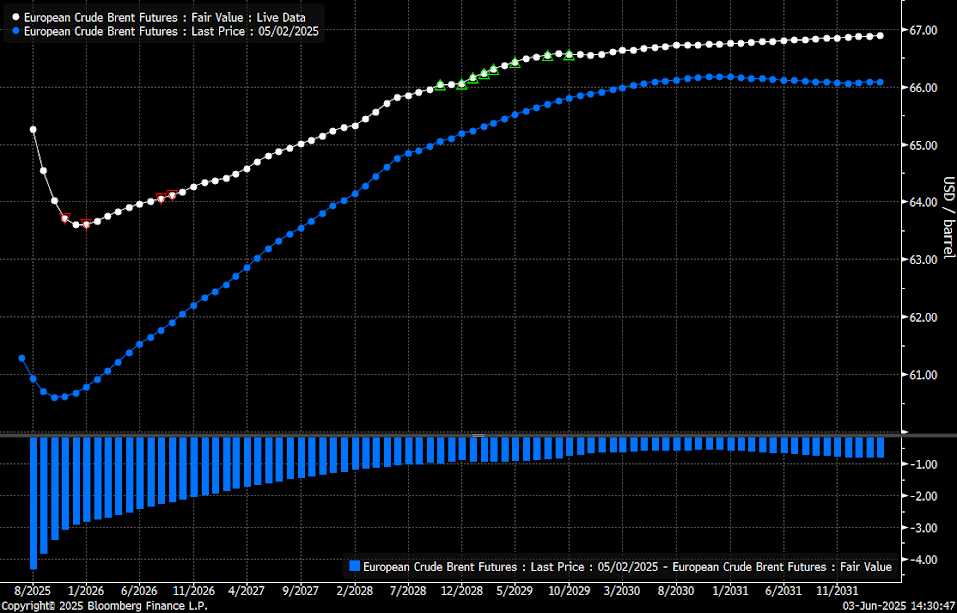

We’re seeing extreme short-term backwardation in both Brent and WTI crude oil, which points to a tight physical market. However, looking at the long term, there’s moderate contango. This suggests that while there’s potential for short-term price increases, prices should remain under pressure in the longer term. Source: Bloomberg Finance L.P.

Natural gas:

- Natural gas prices are reacting to significantly higher temperatures in the US, particularly in the western part of the country. Higher-than-standard temperatures suggest that there may be increased demand for gas to produce electricity for air conditioning or fans.

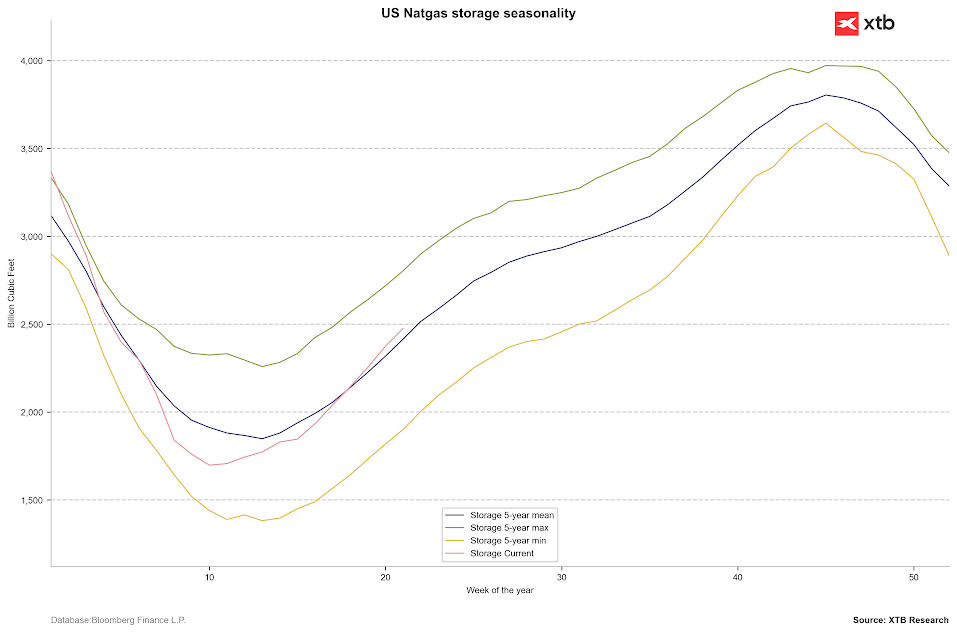

- Gas inventories continue to show significant increases. Last week’s data revealed a build of 101 bcf, in line with expectations. However, inventories are still below last year’s levels but slightly above the levels presented by the 5-year average.

Inventories are now exceeding the 5-year average, but concurrently, we’re observing a clear increase in electricity demand and a decrease in natural gas production in the US. Source: Bloomberg Finance LP, XTB Research

We are currently seeing a noticeable decline in US production. However, this is being offset by a decrease in exports, which means that inventory builds could remain around 100 bcf in the coming weeks. Source: Bloomberg Finance LP, XTB Research

Gas prices are retreating slightly after yesterday’s strong gains. Key support remains around $3.5/MMBTU, while a potential target in the case of significant temperature increases is the $3.9-4.0 range, followed by $4.5-5.0/MMBTU. Source: xStation5

Cocoa:

- Favorable weather in West Africa over the weekend led to a significant price pullback during Monday’s trading session for cocoa, though the $10,000 per ton mark was tested.

- Rainfall that supports crop growth is expected to continue this week.

- During the second session of June, losses are being recovered, with prices now trading near their late May close, about $220 away from the $10,000 per ton level.

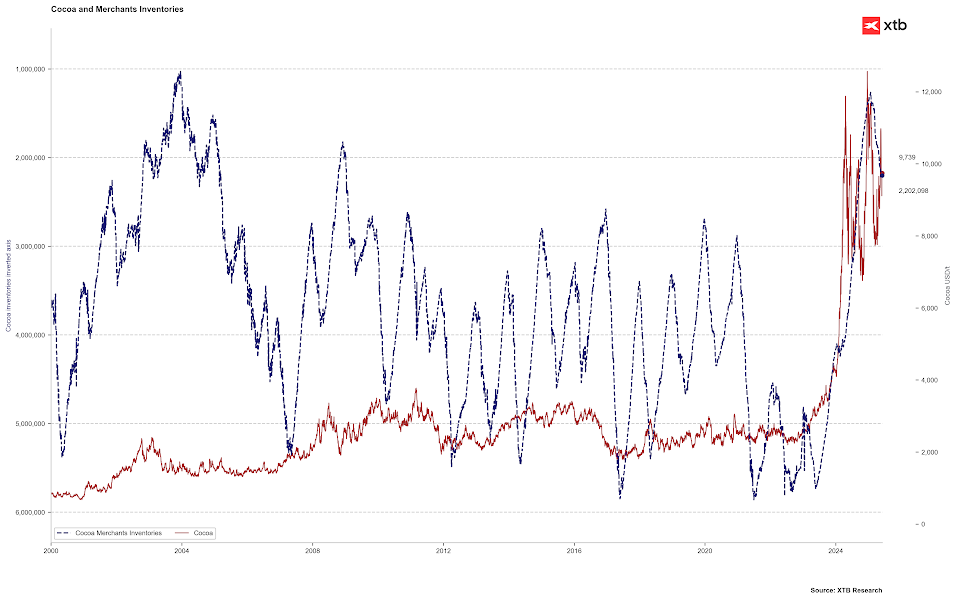

- Cocoa inventories on exchanges continue to increase, now exceeding 2.2 million tons. This is a notable recovery from the 20-year lows of 1.26 million tons reached in January.

- However, cocoa deliveries to ports in Côte d’Ivoire have distinctly decreased. Since the start of the marketing year in October, delivered cocoa is only 6.7% higher year-over-year, a sharp contrast to December’s 35% oversupply compared to the previous year.

Cocoa inventories continue to show strong increases, though when viewed over recent years, they still remain extremely low. Source: Bloomberg Finance LP, XTB Research

On the other hand, we are observing declines in inventories in Europe, which is the largest cocoa market globally. Source: Bloomberg Finance LP, XTB Research

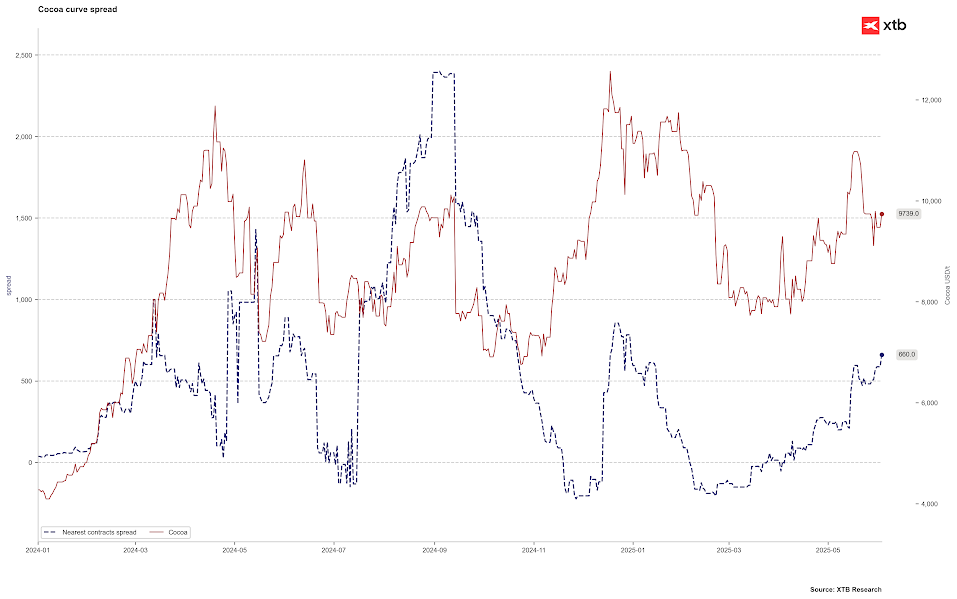

We also see that backwardation (the difference between the current and next contract) has increased to over $600, which signifies significant tension in the physical market. Previously, with such high backwardation, prices were above $12,000 per ton. Source: Bloomberg Finance LP, XTB Research

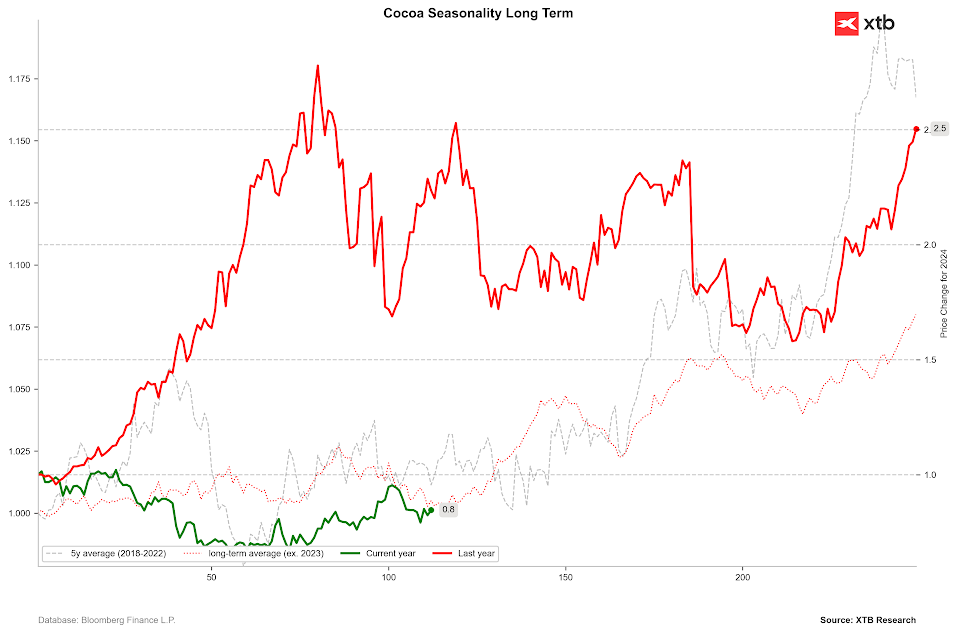

After a weak start to the year, cocoa is beginning to regain its luster. If long-term seasonality is any guide for prices, we should expect increases in the near future. Source: Bloomberg Finance LP, XTB Research

Sugar:

- Concerns about excessive oversupply are putting further downward pressure on sugar prices.

- The organization representing Indian sugar producers (India is the world’s second-largest producer) indicates that production in the current 2025/26 season will increase by 19% year-on-year to 35 million tons. FAS USDA’s forecasts align with this, projecting production at 35.3 million tons.

- Due to this massive increase in production, India is now allowing the export of sugar this season. This is a shift from 2023, when India imposed strict export restrictions to combat high domestic prices.

- At the end of May, the USDA released its semi-annual report on global sugar market fundamentals, which revealed that production is expected to grow by 4.7% year-on-year in the 2025/26 season to 189.32 million tons, with an anticipated surplus of a staggering 42 million tons of sugar.

- FAS USDA also points out that production in Brazil, the world’s largest sugar producer, is projected to increase by 2.3% year-on-year this season, reaching 44.7 million tons.

- This strong growth in sugar production for the 2025/26 season is attributed to favorable weather and a reduction in demand for other sugarcane products, primarily biofuels.

We are currently observing a clear signal of undervaluation relative to the 1-year average and close to excessive undervaluation relative to the 5-year average. Source: Bloomberg Finance LP, XTB Research

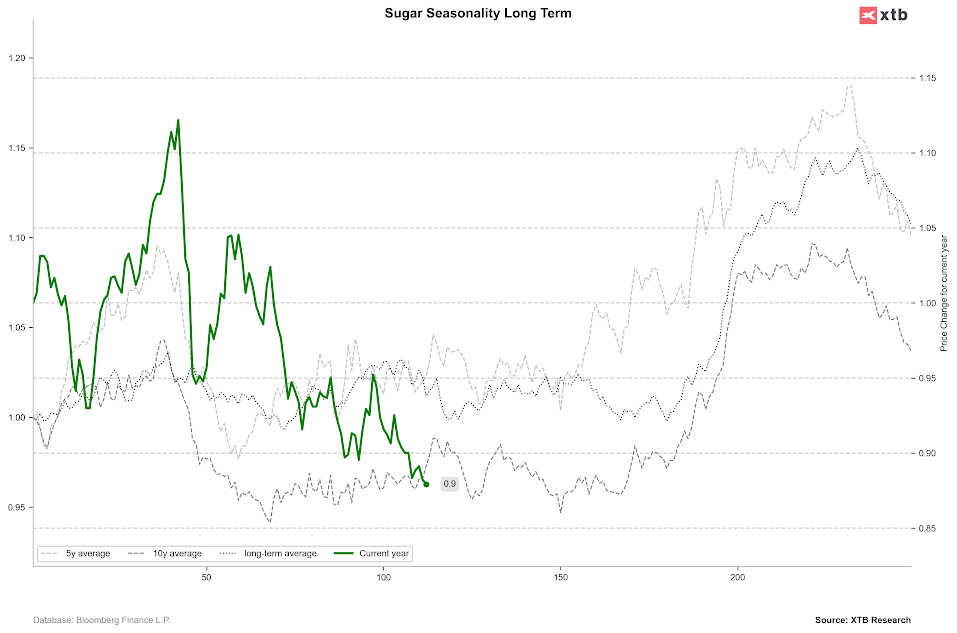

Seasonality in sugar indicates a consolidation phase for another 2-3 months. Source: Bloomberg Finance LP, XTB Research

Sugar prices are currently at a very important support level, around the 61.8% Fibonacci retracement of the last major upward wave. Source: Bloomberg Finance LP, XTB Research

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.